Table of Contents

Introduction

Welcome to the Bricks and Risk blog! Today we dive into the world of owner financing and mortgage note investing as discussed in our recent interview with Nick, founder of Sell My San Antonio House. If you’ve ever wondered how to create predictable, passive income without the hassles of rental property management, you’re in the right place. Over the next 2,000 words, we’ll cover Nick’s journey, core philosophies, practical tips, and the mindset shifts that can transform your real estate investment strategy.

Understanding Owner Financing and Mortgage Notes

Owner financing means that you act as the bank—the buyer makes monthly mortgage payments directly to you. Instead of managing tenants, handling repairs, or dealing with vacancies, you simply collect the payment.

Key Components

Loan Term: Typically set up like a traditional mortgage—15, 20, or 30 years.

Interest Rate: Fixed, with no balloons or prepayment penalties.

Servicing: Payments are collected by a third-party servicer, with escrow for taxes and insurance.

This structure gives you predictability and passivity, as Nick found after years of rental management and fix‑and‑flip deals.

Why Choose Mortgage Notes Over Rentals?

Nick’s transition from rental properties to mortgage notes centered on control and consistency:

Reduced Management Burden

No tenant turnover calls

Fewer maintenance headaches

No property taxes or insurance to handle directly

Predictable Cash Flow

You know exactly how many payments are needed to hit your income goals

Lower variance month to month

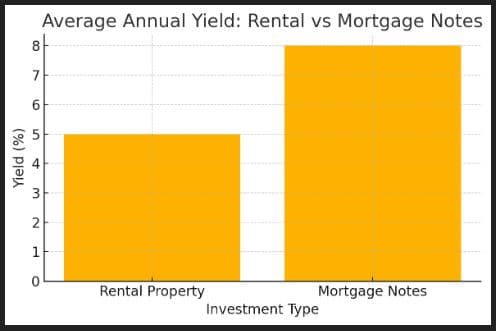

Higher Average Yields

The table and graph below illustrate a comparison of average annual yields. -->

Rental Property: ~5% annual yield

Mortgage Notes: ~8% annual yield

Building Long-Term Relationships

Unlike short‑term lenders, Nick emphasizes a decades‑long commitment to buyers and partners. He says:

“You’re going to be with me for the next 15, 20, 30 years, right?”

This perspective influences:

Deal structuring for sustainability

Client communication focused on trust and authenticity

A reputation that drives referrals and repeat business

Problem-Solving as a Core Value

Real estate investing isn’t just about profit—it’s about relieving burdens:

Buying houses at a discount to help sellers in distress

Providing homeownership to credit‑invisible buyers

Celebrating life‑changing closings, often with tears of joy

“That burden just happened to be in a house.”

Nick’s empathy-driven approach turns transactions into transformative experiences.

Hiring and Managing the Right Team

Scaling a business means learning the hard way about people:

Hiring: Identifying skill sets and culture fits

Firing: Letting go of contributors who aren’t the right match

Mentorship: Learning positive and negative lessons from previous bosses

“I knew for years this was not the right fit…but I kept paying her. That’s not the right way to run a business.”

The takeaway: Invest in people and align roles with strengths.

Setting Goals, Finding Your Why, and Cultivating Grit

Goal‑setting is more than wishful thinking:

Define short-, medium-, and long-term targets

Clarify your personal “why” to power through challenges

Measure daily actions against those goals

“Everything is hard. If you know your why, it will push you through.”

Concrete goals + compelling purpose = sustainable momentum.

The Power of Personal Responsibility

Nick lives by Stephen Covey’s words:

“I am not a product of my circumstances. I am a product of my decisions.”

Instead of excuses—“I don’t have the right background”—focus on “What actions can I take today?” This mindset shift unlocks unlimited potential.

Links to Additional Resources

For further reading on real estate investing and financing:

Frequently Asked Questions

Q1: What is the main benefit of mortgage note investing?

A: Predictable, passive cash flow with minimal management—no tenant calls or repair coordination.

Q2: How long are seller-financed loan terms typically set?

A: Usually 15, 20, or 30 years, mirroring conventional mortgages, with no balloon payments or prepayment penalties.

Q3: Do buyers need good credit to qualify?

A: No—many buyers have solid incomes but little to no credit history, making traditional loans inaccessible.

Q4: How do I ensure my notes are serviced properly?

A: Use a licensed third‑party servicer for collections, escrow management, and county recording.

Q5: Can I mix rentals with mortgage notes?

A: Yes—both strategies can coexist, but focus on the model that best aligns with your passivity and yield goals.